Nigeria Incentive-Based Risk Sharing System for Agricultural Lending (NIRSAL) kicked off a new national Microfinance Bank (MFB) exclusively owned by the Central Bank of Nigeria to cater to over four hundred thousand Micro, Small and Medium Enterprises (SMEs). NIRSAL Microfinance Bank is currently a leading CBN licensed financial institution in Nigeria with a focus of providing citizens of the country basically in the agricultural sector with facilities for a free flow of reasonable finance and investments. So, if you want NIRSAL loan, here is what you should know about NIRSAL Microfinance Bank (MFB) Loan.

The non-banking institution offers a wide range of loans including the NIRSAL Covid-19 loan that can be used for diverse purposes. Loan rates offered are with very minimal interest rates, and they also channel their efforts into redefining the agribusiness sector and all activities revolving around it in the country through repricing, measuring, and sharing credit risks in the sector.

The NIRSAL Microfinance Bank has a targeted 774 branches projected to be located in all local governments across the country. A few branches have been created and more are expected to be in place soon. The bank with a capital base of N5 billion will be efficient in giving support to the CBN in actualizing its 2020 80% financial inclusion. It largely has a 5-year repayment period with a moratorium of two years.

NIRSAL Microfinance Bank Contact Information

Website: nfmb.com.ng

info@nfmb.com.ng

Phone number: +2347041800003

Address: House 1, Plot 103/104, Monrovia street, Wuse 2, Abuja.

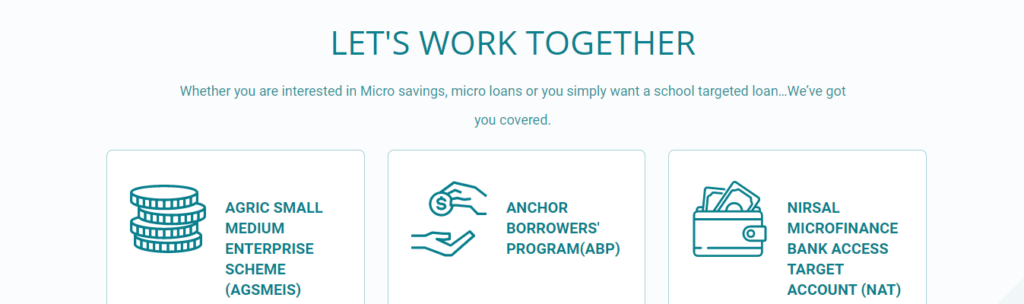

NIRSAL Microfinance Bank Products

NIRSAL provides its customers with the best financial and non-financial products and services to meet their needs. These products and services include:

1. Anchor Borrowers’ Program

This program is channeled towards initiating and fostering a connection between processing sector corporations and small-scale farmers who trade essential commodities in the Agricultural sector.

2. The Agric, Small Medium Enterprise Scheme (AGSMES)

Customers in small and medium-scale enterprises are opened to receive huge loans for up to N10 million with this NIRSAL loan scheme. Businesses that fall in this category are those involved in the Industrial & Manufacturing (automobiles, agriculture & allied Processing), Hospitality (catering & event management), creative & art industries (apparel, fashion, textile, beauty, arts & entertainment), and Information & Communication Technology (media & publishing and telecommunication).

These loans only receive interest rates of less than 10%, and without collateral security.

3. NIRSAL Microfinance Bank Access Target Account

The NIRSAL Microfinance Bank Access Target Account is a savings scheme that is channeled towards private individuals, micro, small, and medium-scale enterprises. So, if you are looking to develop a good saving culture, this scheme is very suitable.

It naturally runs for a given period to meet a particular financial purpose. Customers of this institution receive support to save for diverse purposes, such as purchase of business equipment, goods, rent, and perhaps festivities.

As a customer, your account has a predetermined limit which means that you only have a brief figure of limited withdrawals allowed on the account based on instructions previously given. The account only has a N1000 opening balance and N500 must be retained as minimum balance.

Documents Required For NIRSAL Loan Application

There are certain documents expected to be provided before you can be eligible for NIRSAL Microfinance Bank loan, they include the following:

1. Loan application letter

2. A copy of your employment letter

3. Current utility bill of the applicant and the guarantor

4. A pay slip

5. A guarantor form

6. Six months of your bank account statement

7. 2 passport photographs

8. Your staff Identity card

9. Other valid means of Identification such as your driver’s license, Permanent voter’s card, International passport, or National Identity card.

10. Bank verification number (BVN)

How Does NIRSAL Microfinance Bank Loan Work?

Step 1: You are to receive the required training with an Entrepreneurship Development Center (EDC) that is certified by the Central Bank of Nigeria (CBN)

Step 2: Apply for a loan at the bank through the assistance of the Entrepreneurship Development Institute to provide all required documents for securing the projected loan.

Step 3: Get your funds. They are generally credited into the direct accounts of the beneficiaries. If you are found unqualified, you’ll receive the necessary feedback.

Step 4: Receive support services for your business through the help of the Entrepreneurship Development Institute. You’ll be supported with implementing things such as implementing business plans and other support services commercially.

Step 5: Get you business up and running by selling products and rendering services to help you pay the loan and also make profit.

Step 6: Pay back your loan. Keep all necessary records of your sales and business expenses to maximize profits and settle your loan.

Note that the loan scheme is specifically designed to be of easy access to applicants and the process is entirely automated. From submitting your application to receiving funds generally takes between 6 to 8 weeks in total.

Eligibility For NIRSAL Microfinance Bank Loan

1. The bank assesses the applicant’s capacity to get a loan through their business history by checking out the total account statement turnover with the banks and others. But then, this isn’t the only tool they make use of to determine the eligibility of a customer. Where the applicant’s account statement raises any fundamental issue the bank will expectedly make appropriate decisions.

2. NMFB Customers that have agreed with giving access to the Bank’s Credit unit into their financial records.

3. Customers of the bank must reveal that the loan request the level of sales proceeds that can be viewed in the account statement turnover. In addition, the customer’s books (ledger) must be able to justify the figures.

4. The applicant must reveal evidence of opportunity cost or the adverse effect caused by the COVID-19 pandemic.

Pros of NIRSAL Loans

i. The financial institution offers very competitive loan rates.

ii. They have loan offerings that are of a wide range.

Cons

i. There are some loans that require a guarantor to become accessible.

ii. Huge loans require so much paperwork.

iii. Loan recipients are to engage in compulsory training sessions.